When you need to file an insurance claim for damaged, stolen, or lost property, your insurer will ask for a detailed list of what you lost and proof of its value. For most people, this is an impossible task. Without a pre-existing record, you are forced to rely on memory alone, which is often incomplete, especially after a stressful event.

An incomplete claim means you may not receive the full compensation you are entitled to under your policy. A comprehensive home inventory is the single best tool to protect your financial interests and ensure a smooth claims process. This guide will walk you through how to properly document your possessions, determine their value, and create the evidence you need to substantiate your claim.

A home inventory is your primary evidence when filing an insurance claim. Insurers require proof of ownership and value before they will issue a payment.

Did You Know? Research shows that homeowners relying on memory can typically recall only 20-40% of their belongings after a loss.

Consider your kitchen alone—from small appliances and cookware to every dish and utensil. Now multiply that across every room, closet, and storage space in your home. Your insurance policy requires you to submit a “proof of loss” that itemizes everything. Vague descriptions like “furniture” or “clothing” will only result in minimal payouts. The burden of proof is on you, the policyholder, to document what you owned and what it was worth. A pre-loss inventory provides organized, credible evidence that simplifies this process and strengthens your claim.

Creating a thorough inventory requires a systematic approach. Follow these steps to ensure you capture everything of value.

Select a format that you will be able to maintain easily. You can use spreadsheet software like Microsoft Excel or Google Sheets, or dedicated home inventory apps like Sortly or Encircle. A simple video walkthrough is another quick option. For high-value collections or complex estates, a professional inventory service can provide comprehensive documentation and valuation.

Pro Tip: Always store your inventory securely off-site in cloud storage, a safety deposit box, or with a trusted relative. An inventory that is destroyed along with your property is of no use.

A methodical approach prevents omissions. Start at your front door and work your way through your home. In living and family rooms, document furniture, electronics, artwork, and decor. In the kitchen, be sure to include not just major appliances but also smaller items like cookware and dishes. For bedrooms, list all furniture, bedding, and clothing. Don’t forget bathrooms, home offices, and storage areas like garages, which often contain tools and sports gear. Finally, document outdoor items like patio furniture and grills if they are covered by your policy.

For each item, record key details such as its name, brand, model, and a brief description. Note the purchase date, original price, and any serial numbers, which are crucial for electronics and appliances. Also, document the item’s condition (e.g., new, good, fair), as this is important for determining its value. Wherever possible, attach or reference supporting documents like receipts, warranties, or credit card statements.

Visual documentation is powerful evidence. Take clear photos of your most valuable items from multiple angles, including close-ups of brand names, model numbers, and serial numbers. For collections of jewelry, art, or antiques, photograph each piece individually as well as in a group.

Pro Tip: When recording a video walkthrough, open every closet, drawer, and cabinet. This helps capture the contents you might otherwise forget.

A home inventory is a living document that requires regular updates. We recommend reviewing it annually when you review your insurance policy. You should also update it immediately after major purchases, after receiving inherited property, or when you sell or dispose of significant items. A quick 30-minute review each year is a small investment that maintains the accuracy and value of your records.

If you need to file a claim without a pre-existing inventory, you will have to reconstruct a list of your possessions. While challenging, this process is essential.

First, gather all available financial records. Review several years of credit card statements, bank records, and online purchase histories. Next, look through all photos and videos taken inside your home, paying close attention to items visible in the background. With this information, work room by room and use categories as prompts to jog your memory.

Be Specific: Vague descriptions get minimal payouts. Instead of “couch,” write “Gray fabric L-shaped sectional sofa, 8x6 feet, purchased from Ashley Furniture, approx. 3 years old.” This level of detail justifies a higher valuation and reduces disputes.

Accurate valuation is critical for receiving fair compensation. The method you use will depend on your insurance coverage.

Your policy will provide one of two types of coverage for personal property. Check your policy declarations to see which coverage you have, as this dictates how you should value your items.

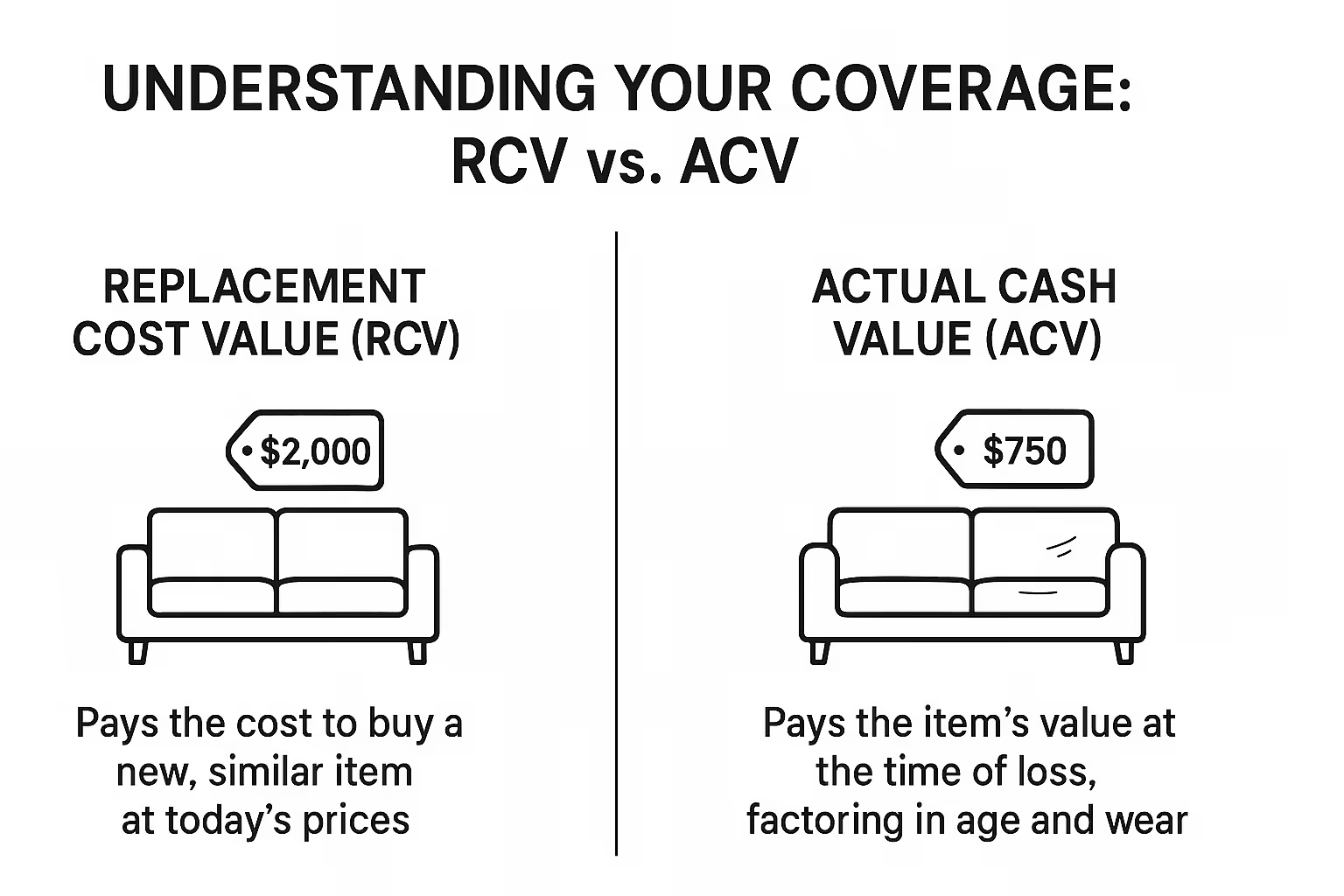

Replacement Cost vs Actual Cash Value

For RCV claims, research the current retail price of a new, comparable item. For ACV claims, you must calculate the depreciated value by researching prices for similar used items on sites like eBay or Facebook Marketplace. For bulk items like clothing or kitchen utensils, insurers may accept category-based estimates (e.g., “20 dress shirts at $50 each”).

For high-value items, typically those worth $1,000 or more, insurance companies often require an independent professional appraisal. This requirement applies to a broad category of assets, including jewelry and fine watches, fine art, antiques and collectibles, valuable musical instruments, Oriental rugs, and specialized collections such as firearms and wine.

A qualified appraisal must come from a certified professional with expertise in the specific type of property. The appraiser must be independent and provide a detailed report that documents their methodology, including a full description of the item, high-quality photos, and a clear statement of value. Professional appraisals provide authoritative documentation that streamlines claims and eliminates disputes over value.

How often should I update my home inventory?

Update your inventory at least once a year. You should also make immediate updates after purchasing or selling expensive items to ensure your coverage limits remain adequate.

Do I need separate insurance for high-value items?

Yes. Most homeowners' policies have sub-limits, often between $1,500 and $2,500, for categories like jewelry or fine art. To insure items for their full value, you need a scheduled personal property endorsement(also called a floater or rider). A professional appraisal is required to schedule an item.

What if I don’t have receipts?

Receipts are helpful but not required for most items. Credit card statements, warranties, and photos can all serve as proof of ownership. For high-value items, a professional appraisal establishes both ownership and value.

Can I file a claim if I don’t have an inventory?

Yes, but the process is far more difficult, and you risk a lower settlement. You will have to reconstruct your losses from memory, a process where most people significantly underestimate what they owned. For more tips, visit our blog.

How long should I keep appraisals?

Keep current appraisals for as long as you own the item and it remains insured. We recommend updating appraisals every 3-5 years to reflect changes in market value.

The time you spend creating an inventory now can save you thousands of dollars and immense stress later. For your most valuable possessions, a professional appraisal provides the authoritative documentation needed to secure full insurance coverage and ensure a smooth claims process.

If you are uncertain about the value of your artwork, jewelry, antiques, or other valuable property, don’t guess. A certified appraisal eliminates disputes and gives you confidence in your coverage.

Ready to protect your valuable possessions with professional documentation? Contact our certified appraisers for insurance appraisals that meet all insurer requirements. We provide detailed, compliant reports for all types of personal property. Document them properly. Value them accurately. Protect them completely.