Many people assume their homeowners insurance fully protects all their belongings, but this is rarely the case. Standard policies contain specific coverage limits—or sub-limits—for high-value items like jewelry, art, and collectibles. If a treasured item’s value exceeds this limit, you could be left with a significant financial gap after a loss.

A scheduled personal property floater is specialized insurance designed to close that gap. It provides the comprehensive protection your valuables need but don’t receive from a standard policy. This guide explains what a scheduled floater is, how it works, and why it’s an essential tool for protecting your most important possessions.

A standard homeowners or renters policy is designed to cover your home and general belongings, but it falls short when it comes to valuables. To manage risk, insurance companies place low coverage limits on certain categories of items. For example, a typical policy might only cover jewelry up to $1,500, firearms up to $2,500, and fine art up to another low limit, regardless of their actual worth.

This means if you own an engagement ring appraised at $10,000, your policy’s $1,500 sub-limit leaves you personally responsible for the remaining $8,500 if the ring is lost or stolen. This is a significant financial risk you may not even realize you’re taking.

Key Takeaway: A standard policy’s $1,500 jewelry limit means you’re personally responsible for the remaining $8,500 on a $10,000 ring. This is the coverage gap a floater is designed to fill.

To address this gap, a scheduled personal property floater provides specific, itemized coverage. The term “scheduled” means each valuable item is individually listed on your policy with its professionally appraised value, creating a clear record of what’s insured and for how much. The term “floater” means the coverage follows your belongings wherever they go—whether at home, in another city, or traveling with you overseas.

By scheduling an item, you insure it for its full worth. This coverage is also typically “all-risk,” meaning it protects against a wider range of events than a standard policy, including accidental damage or mysterious disappearance.

This specialized coverage offers several critical benefits that standard policies lack, making it a necessary tool for anyone with high-value possessions.

First, it provides a full value payout with no depreciation. Unlike a standard policy that pays “actual cash value,” a scheduled policy pays the full, agreed-upon value listed in your policy. You can learn more about the differences between replacement value vs. fair market value on our blog. If your watch scheduled for $8,500 is stolen, you receive $8,500, ensuring you have the funds to replace it without dispute.

Second, you gain broader “all-risk” protection. Standard policies typically only cover “named perils” like fire and theft. They won’t cover you for accidental damage, like dropping your camera, or mysterious disappearance, like a ring that simply goes missing. “All-risk” coverage protects against all causes of loss unless a cause is specifically excluded, offering far more comprehensive protection for real-life situations.

Pro Tip: “All-risk” coverage protects against losses standard policies don’t, like accidentally dropping your camera or a ring that simply goes missing.

Finally, scheduled floaters offer worldwide coverage and often have no deductible. Your valuables are protected anywhere in the world, and if you file a claim, you generally receive the full scheduled amount without having to pay a deductible first.

You can schedule almost any valuable item whose worth exceeds your policy’s sub-limits, as long as you can document its value with a professional appraisal. Commonly scheduled items include high-value jewelry, such as engagement rings and luxury watches, as well as fine art like paintings and sculptures. You can also schedule extensive collections of rare coins, stamps, or vintage wine. Other categories include musical instruments, antiques like rare books, and specialty items such as high-end cameras or designer handbags. The key factor is whether an item’s value is high enough to create a coverage gap and whether you can provide an appraisal to confirm its worth.

Once you decide to schedule your property, you have two primary options for obtaining coverage.

The first is a scheduled personal property endorsement, which is an add-on or “rider” to your existing homeowners policy. This is often the simplest and most cost-effective choice. The main drawback is that any claim you file goes on your homeowners insurance record, which could potentially impact your rates.

The second option is a standalone Personal Articles Floater (PAF), which is a separate, independent policy just for your valuables. A key advantage here is that claims filed on a PAF do not affect your homeowners policy. This option offers greater flexibility and is ideal for those with extremely high-value collections.

Before an insurance company will schedule your property, you must provide a professional appraisal. This isn’t just a formality—it protects both you and the insurer by establishing a clear, agreed-upon value before a loss occurs.

An insurance-acceptable appraisal must be USPAP-compliant and completed by a qualified expert. It must state the item’s replacement value and include a detailed description, high-quality photos, and market research. At AppraiseItNow, we specialize in providing USPAP-compliant appraisals designed specifically for insurance. Because market values can change, most insurers require you to update your appraisals every 3 to 5 years.

Important Note: A professional, insurance-acceptable appraisal is not optional. It is a mandatory requirement from insurers before they will schedule your property for its full value.

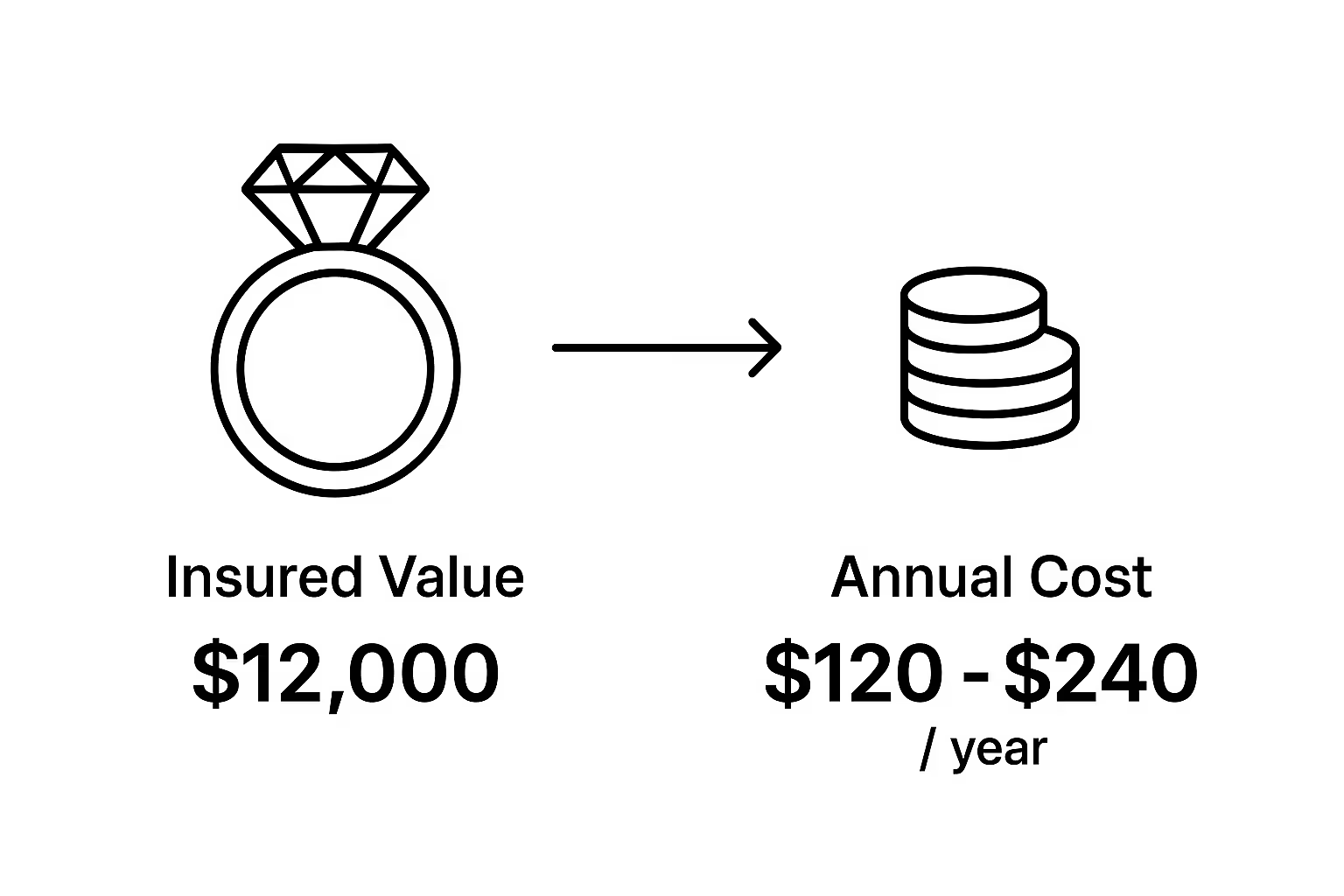

Fortunately, this comprehensive protection is quite affordable. Premiums are typically calculated as a small percentage of the item’s insured value, usually between 1% and 2% per year. You can find more information on our pricing page. For example, a $12,000 engagement ring might cost $120 to $240 per year to insure. While it is an additional cost, it is minimal compared to the financial devastation of losing a valuable item without proper coverage.

Q: Do I need an appraisal for every item I want to schedule?

A: Yes, insurance companies require a professional, USPAP-compliant appraisal to establish an agreed-upon value for each high-value item you schedule.

Q: What happens if my item increases in value?

A: You are only covered for the scheduled value. If your item appreciates, you should get an updated appraisal and adjust your coverage amount to avoid being underinsured. Most insurers require updated appraisals every 3-5 years.

Q: Is my scheduled property covered worldwide?

A: Generally, yes. Most floaters provide worldwide coverage, but you should always review your policy’s territorial limits before traveling abroad with valuables.

Q: Does this coverage have a deductible?

A: Most scheduled property policies have a $0 deductible, which is a major advantage. Some policies offer an optional deductible in exchange for a lower premium.

Your valuable possessions are more than just financial assets; they are symbols of milestones, family history, and personal passion. A standard insurance policy was not designed to protect them fully, leaving you exposed to significant financial loss.

Scheduled personal property coverage closes this gap. The process begins with a professional appraisal—an essential step that provides the foundation for proper protection.

Don’t wait until after a loss to discover your coverage is inadequate. Take these steps today:

Ready to properly protect your valuables? The first step is a professional appraisal. At AppraiseItNow, we provide USPAP-compliant appraisals that insurance companies trust. Our nationwide network of certified experts ensures you receive accurate, detailed valuations for your jewelry, fine art, antiques, and collectibles.

Request a quote or schedule your appraisal with us today. You can also contact us with any questions. Secure the peace of mind that comes from knowing your most treasured possessions are properly protected.