IRS-qualified appraisals for donated technology equipment, meeting the Form 8283 Section B threshold above $5,000. AppraiseItNow provides USPAP-compliant fair market value reports for computers, servers, and networking gear to support your deduction.

Best in class appraisers across asset types

.avif)

Joe Kattan

Aron Blue

Technology Equipment Appraisals for Charitable Donations

AppraiseItNow provides qualified appraisals of donated technology equipment for donors who need to substantiate IRS deductions under federal tax rules. When the fair market value of donated tech equipment exceeds $5,000 for a single item or group of similar items in a tax year, the IRS requires a qualified appraisal and a completed Form 8283 Section B, signed by both the appraiser and the receiving organization. Our equipment valuation practice covers everything from individual workstations to large-scale server infrastructure, with appraisals completed within the IRS-required window of no earlier than 60 days before the donation date.

We deliver appraisals both online and onsite across the United States, giving donors flexibility regardless of where equipment is located. Our IRS charitable contribution appraisals are completed by credentialed appraisers holding designations through organizations including ASA and ISA, with each report fully USPAP-compliant and defensible in the event of an audit. Our mission is to deliver defensible, USPAP-compliant valuations with exceptional speed, professionalism, and client service.

Technology Equipment We Appraise for Charitable Giving

AppraiseItNow appraises a wide range of donated technology assets for individual donors, businesses, and institutions. Specific categories include:

- Desktop computers, workstations, and all-in-one units

- Laptops, tablets, and mobile computing devices

- Servers, rack-mounted systems, and data center hardware

- Networking equipment including routers, switches, and firewalls

- Telecommunications hardware such as PBX systems and VoIP infrastructure

- Printers, scanners, copiers, and multifunction devices

- Audio-visual and presentation technology including projectors and display systems

- Point-of-sale systems and retail technology hardware

- Medical and scientific computing equipment

- Peripheral devices and accessories donated as part of a larger technology package

How Our Technology Equipment Appraisal Process Works

- Appraisers conduct a physical inspection or a thorough remote review using photos, serial numbers, purchase records, and maintenance documentation, then research current market data including comparable sales, dealer pricing, and auction results to establish fair market value as of the donation date.

- Each appraisal report includes a detailed description of the equipment, its condition and operational status, the valuation methodology applied, supporting market data, and the appraiser's signed declaration required for Form 8283 Section B.

- Appraisers account for technology-specific factors that affect value, including age, model generation, functional obsolescence, upgrade history, and current demand in the secondary market for used hardware.

- All appraisers are credentialed through recognized professional organizations such as ASA or ISA, are independent of the donor and donee, and meet IRS qualification standards for qualified appraisers under Treasury Regulation 1.170A-17.

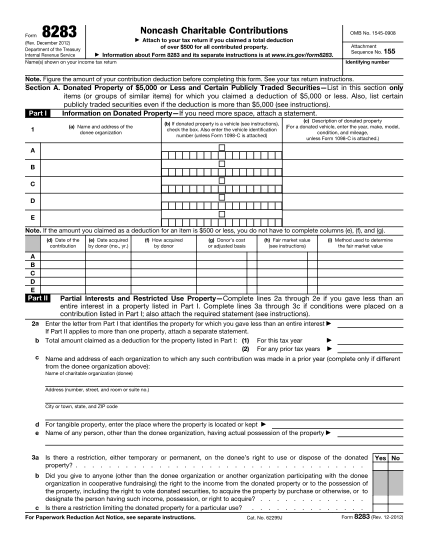

IRS Form 8283 Appraisals Required for Large Non-Cash Charitable Donations

Comprehensive qualified appraisals determining fair market value for non-cash donations exceeding $5,000, developed under USPAP standards and aligned with IRS Form 8283, Section B requirements.

What is IRS Form 8283?

IRS Form 8283, Noncash Charitable Contributions, is required when a taxpayer claims a deduction for donated property exceeding $500, and it becomes significantly more detailed when the value of donated non-cash property exceeds $5,000.

For contributions over $5,000 (other than certain publicly traded securities), the IRS generally requires a Qualified Appraisal prepared by a qualified appraiser. In these cases, the donor must complete Section B of Form 8283, and the appraiser must complete and sign Part IV (Appraiser Declaration) to confirm the appraisal meets IRS standards.

AppraiseItNow Performs 8283 Appraisals

AppraiseItNow is an expert in preparing qualified appraisals for filing of IRS Form 8283. We work with donors and their advisors to establish defensible fair market value in accordance with USPAP and IRS requirements, including support for Form 8283, Section B reporting and the appraiser declaration in Part IV.

Our credentialed appraisers provide valuation support across major asset categories, including:

- Personal Property Appraisals

- Fine Art Appraisals

- Machinery & Equipment Appraisals

- Business Valuations

- Inventory Appraisals

- Bullion & Precious Metal Appraisals

- Vehicle Appraisals

- Cryptocurrency Appraisals

Whether the asset is readily marketable or complex and illiquid, we provide independent, well-supported fair market value opinions designed to withstand scrutiny and support proper charitable reporting.

5-Star Valuation Services, Loved by Hundreds

How much does a Technology Equipment appraisal cost?

Appraisal Type

Standard Fee Range

Pricing By Volume

What Drives Cost?

.svg)

View all Locations

What does a technology equipment appraisal for charitable donation involve?

A charitable donation appraisal for technology equipment determines the fair market value of your donated assets, such as computers, servers, networking gear, and peripherals, as of the date of contribution. The process includes a review of the equipment's condition, age, functionality, and market comparables, resulting in a USPAP-compliant written report suitable for IRS submission. The appraiser also signs Form 8283 Section B, which must accompany your tax return when claiming deductions above $5,000.

When do you need a qualified appraisal for donated technology equipment?

A qualified appraisal is required when the aggregate fair market value of donated technology equipment exceeds $5,000 in a single tax year, whether donated to one charity or several on the same effective date. For donations between $250 and $5,000, a written acknowledgment from the receiving organization is generally sufficient. Once the $5,000 threshold is crossed, Form 8283 Section B with an appraiser signature must be attached to your tax return.

What credentials should the appraiser have?

The appraiser must be independent, experienced in valuing technology equipment, and credentialed through a recognized professional organization such as the International Society of Appraisers (ISA) or the American Society of Appraisers (ASA). AppraiseItNow appraisers hold credentials through ISA, ASA, AAA, CAGA, AMEA, and NEBB. The appraiser must also have no financial interest in the donation and must declare their qualifications directly on Form 8283 Section B.

How is technology equipment valued for charitable donation purposes?

Technology equipment is valued using fair market value methodology, which reflects the price a willing buyer and seller would agree upon in an open market. Appraisers research comparable sales of used equipment, current dealer quotes, and auction results while accounting for the item's condition, age, functionality, and technological obsolescence. The valuation is tied to the exact donation date, which is the date of title transfer to the charity.

Are AppraiseItNow's appraisals USPAP-compliant?

Yes, all AppraiseItNow appraisals are fully USPAP-compliant and prepared to IRS qualified appraisal standards, including proper valuation date documentation, methodology disclosure, appraiser credentials, and a non-contingent fee declaration. These standards are specifically required for charitable donation deductions exceeding $5,000. Following these requirements significantly reduces the risk of IRS scrutiny or disallowance of your deduction.

How long does a technology equipment appraisal take?

Most remote appraisals are completed in 7 to 10 days. Onsite inspections or larger collections typically take 2 to 3 weeks. Rush service is available for same-day or next-day turnaround if your donation timeline requires it.

How is pricing structured for a technology equipment charitable donation appraisal?

Fees are fixed and quoted before work begins, so you know the cost upfront. Standard USPAP-compliant appraisals start at $295, while IRS-qualified reports for charitable donation purposes start at $395. Most technology equipment appraisals fall in the $695 to $2,200 range, with larger inventories of 50 or more items running $5,000 to $10,000 or more depending on complexity, visit our equipment appraisal page for more detail. Key cost factors include:

- Variety of equipment categories, models, and technical complexity

- Quantity of line items and duplicate SKUs

- Condition differences and whether onsite verification is needed

- Quality of documentation such as photos, serial numbers, and maintenance logs

- Compliance requirements specific to IRS charitable donation purposes

Can you appraise technology equipment anywhere in the US?

Yes, AppraiseItNow provides technology equipment appraisals nationwide. Remote appraisals can be completed using photos, specifications, and documentation you provide, while onsite inspections are available for larger collections or situations requiring physical verification.

Will my appraisal be accepted by the IRS, insurers, or courts?

AppraiseItNow appraisals are prepared to IRS qualified appraisal standards, including proper valuation date, documented methodology, appraiser credentials, and a non-contingent fee declaration, all of which are required for charitable donation deductions above $5,000. While no appraisal firm can guarantee acceptance in every context, following these standards significantly reduces the risk of disallowance. For insurance or legal matters, acceptance depends on the specific requirements of the reviewing party.

Do multiple laptops donated to different charities still count as similar items under IRS rules?

Yes, the IRS treats laptops and other electronic equipment as similar items regardless of how many charities receive them. If their combined fair market value exceeds $5,000 in a single tax year, a qualified appraisal with Form 8283 Section B is required. A single appraisal report can cover all similar items sharing the same donation date, though each donee organization may need a separate Form 8283.

How is fair market value determined for older networking gear in a charitable donation appraisal?

Appraisers research comparable sales of used networking equipment, current dealer quotes, and auction results to establish market value. The evaluation also accounts for the equipment's condition, functionality, age, technological relevance, and maintenance history. The resulting value reflects what a willing buyer and seller would agree upon in an open market, not the original purchase price or replacement cost.

Can the appraisal be completed more than 60 days before the donation date?

No, IRS rules require that the appraisal be completed no more than 60 days before the effective donation date, which is the date of title transfer to the charity. An appraisal prepared outside that window will not meet IRS requirements and cannot be used to substantiate your deduction. Plan your appraisal timeline carefully to ensure the report date falls within the allowable period.

Do monitors and keyboards need an appraisal if their combined value exceeds $5,000?

Yes, monitors and keyboards are considered similar items under IRS rules because they fall within the same generic category of electronic equipment. If their aggregate fair market value exceeds $5,000, a qualified appraisal and Form 8283 Section B are required. The combined value across all similar items, not each piece individually, determines whether the appraisal threshold is triggered.

What should I know about data wiping before having my tech equipment appraised for donation?

Use a certified data destruction service to fully erase sensitive information before donating, and obtain documentation of the process to include in your appraisal records. Proper data erasure protects you and the receiving organization from security and compliance risks after the transfer. Failing to document this step can create liability issues and may complicate the legitimacy of the donation itself.

APPRAISEITNOW APPRAISERS ARE BEST-IN-CLASS & CREDENTIALED BY LEADING APPRAISAL ORGANIZATIONS LIKE THE ISA, ASA, & MORE.