IRS-qualified appraisals for donated mobile homes, meeting Form 8283 Section B requirements for deductions over $5,000. AppraiseItNow provides USPAP-compliant fair market value reports that substantiate your charitable contribution and protect your deduction at tax time.

Best in class appraisers across asset types

.avif)

Joe Kattan

Aron Blue

Mobile Home Appraisals for Charitable Donations

When you donate a mobile or manufactured home classified as personal property to a qualifying nonprofit, the IRS requires a qualified appraisal to substantiate any deduction of $5,000 or more. That appraisal must establish fair market value and be completed no earlier than 60 days before the donation date, with Form 8283 Section B signed by both the appraiser and the donee organization. AppraiseItNow's mobile and manufactured vehicle valuation practice handles exactly this type of assignment, with credentialed appraisers experienced in factory-built housing classified as chattel.

We deliver appraisals both online and onsite across the United States, making the process straightforward regardless of where the home is located. Whether you need a single report for a straightforward donation or documentation for a more complex transfer, our IRS charitable donation appraisal services are built to meet every applicable requirement. Our mission is to deliver defensible, USPAP-compliant valuations with exceptional speed, professionalism, and client service.

Mobile Home Types We Appraise for Charitable Giving

AppraiseItNow appraises a wide range of factory-built homes classified as personal property for donation purposes, including:

- Single-wide mobile homes on owned or leased land, titled as personal property

- Double-wide and triple-wide manufactured homes not converted to real property

- HUD-code manufactured homes built after June 15, 1976, with intact data plates

- Pre-HUD mobile homes built before 1976, often requiring condition-focused analysis

- Park model homes and recreational-use manufactured units

- Mobile homes with original chassis and wheels still attached

- Older mobile homes donated to nonprofit housing organizations or community land trusts

- Manufactured homes in mobile home parks where the land is not included in the donation

- Homes with significant upgrades or additions that affect value relative to base comparables

- Mobile homes in deteriorated or as-is condition donated for demolition or land reclamation purposes

How Our Mobile Home Charitable Donation Appraisal Process Works

- Clients submit details about the home including year, make, size, HUD labeling status, location, and condition, along with the intended donation date and the receiving organization's information. This intake shapes the scope of the assignment from the start.

- A credentialed appraiser, holding designations through organizations such as ISA, ASA, or AAA, researches comparable sales of similar personal property mobile homes, adjusts for condition, age, features, and local market demand, and develops a supportable fair market value conclusion consistent with IRS standards.

- The completed appraisal report includes a full property description, valuation methodology, comparable market data, the appraiser's signed certification, and all information required to complete Form 8283 Section B. Reports are formatted to withstand IRS review and are delivered digitally for easy attachment to your tax return.

- Appraisals are timed to meet IRS deadlines, meaning the report is completed within the window that begins no earlier than 60 days before the donation and no later than the due date of the tax return on which the deduction is claimed, including extensions.

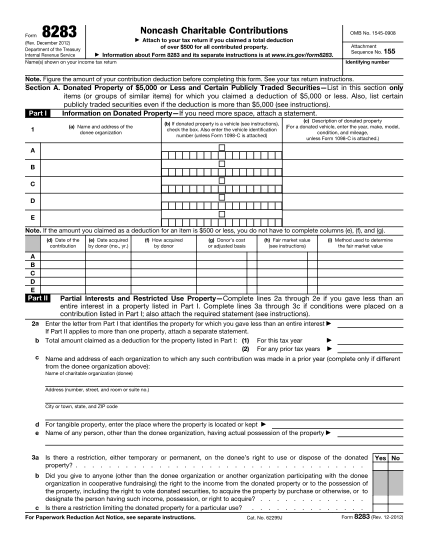

IRS Form 8283 Appraisals Required for Large Non-Cash Charitable Donations

Comprehensive qualified appraisals determining fair market value for non-cash donations exceeding $5,000, developed under USPAP standards and aligned with IRS Form 8283, Section B requirements.

What is IRS Form 8283?

IRS Form 8283, Noncash Charitable Contributions, is required when a taxpayer claims a deduction for donated property exceeding $500, and it becomes significantly more detailed when the value of donated non-cash property exceeds $5,000.

For contributions over $5,000 (other than certain publicly traded securities), the IRS generally requires a Qualified Appraisal prepared by a qualified appraiser. In these cases, the donor must complete Section B of Form 8283, and the appraiser must complete and sign Part IV (Appraiser Declaration) to confirm the appraisal meets IRS standards.

AppraiseItNow Performs 8283 Appraisals

AppraiseItNow is an expert in preparing qualified appraisals for filing of IRS Form 8283. We work with donors and their advisors to establish defensible fair market value in accordance with USPAP and IRS requirements, including support for Form 8283, Section B reporting and the appraiser declaration in Part IV.

Our credentialed appraisers provide valuation support across major asset categories, including:

- Personal Property Appraisals

- Fine Art Appraisals

- Machinery & Equipment Appraisals

- Business Valuations

- Inventory Appraisals

- Bullion & Precious Metal Appraisals

- Vehicle Appraisals

- Cryptocurrency Appraisals

Whether the asset is readily marketable or complex and illiquid, we provide independent, well-supported fair market value opinions designed to withstand scrutiny and support proper charitable reporting.

5-Star Valuation Services, Loved by Hundreds

.svg)

View all Locations

What does a mobile home appraisal for charitable donation involve?

A charitable donation appraisal for a mobile home is a formal, IRS-compliant evaluation that determines the fair market value of the property on the date of contribution. The appraiser examines the mobile home's physical condition, age, size, features, and comparable market data to produce a written report that substantiates the deduction you claim on your tax return. The completed appraisal supports your filing on Form 8283 Section B and must meet all IRS qualified appraisal requirements under USPAP standards.

When is a qualified appraisal required for donating a mobile home?

A qualified appraisal is required when the fair market value of the donated mobile home is $5,000 or more, whether as a single item or as part of a group of similar items aggregating to $5,000 or more in the same tax year. The appraisal must be completed no earlier than 60 days before the donation date and received before the due date, including extensions, of the tax return on which you first claim the deduction.

What credentials should the appraiser have?

The appraiser must hold a professional designation from a recognized appraisal organization such as ISA, ASA, AAA, CAGA, AMEA, or NEBB, and must have demonstrated experience valuing mobile homes or similar personal property. They must follow USPAP standards, have no conflicts of interest with the donor or charity, and sign Form 8283 Section B under penalty of perjury declaring their qualifications.

How is a mobile home valued for charitable donation purposes?

Appraisers use IRS-approved methodologies to determine fair market value, which is the price a willing buyer and seller would agree upon in an open market on the specific date of contribution. The primary approaches include:

- Comparable sales analysis using recent auction results, private sale records, and retail market data for similar mobile homes adjusted for age, size, location, condition, and features

- Cost basis approach using the original purchase price adjusted for depreciation or appreciation

- Expert analysis incorporating the mobile home's structural integrity, physical condition, and current market demand

The final value reflects all relevant factors as of the contribution date, not the purchase date or any other point in time.

Are AppraiseItNow's appraisals USPAP-compliant?

Yes, all AppraiseItNow appraisals are fully USPAP-compliant and prepared by credentialed appraisers holding designations from recognized organizations including ISA, ASA, AAA, CAGA, AMEA, and NEBB. Each report includes the required valuation date, methodology, appraiser credentials, and a non-contingent fee declaration to meet IRS qualified appraisal standards.

How long does a mobile home appraisal take?

Turnaround is typically 3 to 5 days depending on the complexity of the mobile home and the number of assets being appraised. If you have a filing deadline approaching, contact us early so we can confirm timing before you schedule the donation.

What does a mobile home charitable donation appraisal cost?

Fees are scope-based and quoted as a fixed price before work begins. Cost depends on the complexity, size, and purpose of the appraisal, so contact us for a quote or visit our pricing page for general ranges.

Can you appraise mobile homes anywhere in the US?

Yes, AppraiseItNow provides mobile home appraisals nationwide. Whether the property is located in a rural area, a manufactured housing community, or anywhere else across the country, our credentialed appraisers can complete the evaluation.

Will my appraisal be accepted by the IRS, insurers, or courts?

AppraiseItNow appraisals are prepared to qualified appraisal standards, including a defined valuation date, documented methodology, appraiser credentials, and a non-contingent fee declaration. While no appraiser can guarantee acceptance by any authority, following these standards closely mirrors IRS requirements and significantly reduces the risk of a disallowed deduction.

When does donating a mobile home to charity limit my tax deduction?

If the charity plans to auction or resell the mobile home rather than use it directly in its charitable mission, the IRS considers that an unrelated use, and your deduction is limited to the lesser of fair market value or your cost basis. This can result in a substantially lower deduction than the appraised value, so it is worth confirming the charity's intended use before completing the donation.

Can I combine my mobile home donation with other items to reach the $5,000 appraisal threshold?

You can aggregate similar items donated in the same tax year, and if the combined value reaches $5,000 or more, a qualified appraisal is required for the group. However, items that are not similar to each other must each be appraised separately if any individual item is valued at $5,000 or more.

What is the timing rule for getting a mobile home appraisal before claiming a charitable deduction?

The appraisal must be completed no earlier than 60 days before the date you contribute the mobile home and must be in hand before the due date, including extensions, of the tax return on which you first claim the deduction. If you are filing an amended return, the appraisal must be obtained before that amended return is filed.

Who is qualified to appraise a mobile home for a charitable donation write-off?

A qualified appraiser must hold a professional designation from a recognized appraisal organization, have completed relevant coursework and current certifications, and have regular experience valuing mobile homes or similar personal property. They must have no conflicts of interest with the donor or the receiving charity, adhere to USPAP standards, and sign Form 8283 Section B under penalty of perjury.

What documentation do I need beyond the appraisal to claim a mobile home donation over $5,000?

In addition to the qualified appraisal report, you will need:

- Form 8283 Section B signed by the qualified appraiser

- Written acknowledgment from the charity describing the donation and any goods or services received in exchange

- A description of the donated mobile home and the date of contribution

- Records showing how and when you acquired the mobile home, including cost basis documentation

- The donee organization's tax identification number and the appraiser's credentials and tax identification number

Retain all documentation for at least 7 years in case of an IRS audit.

APPRAISEITNOW APPRAISERS ARE BEST-IN-CLASS & CREDENTIALED BY LEADING APPRAISAL ORGANIZATIONS LIKE THE ISA, ASA, & MORE.