IRS-qualified appraisals for donated kitchen appliances, meeting Form 8283 Section B requirements when FMV exceeds $5,000. AppraiseItNow provides defensible fair market value reports for refrigerators, ranges, dishwashers, and more, helping donors maximize their charitable deduction with confidence.

Best in class appraisers across asset types

.avif)

Joe Kattan

Aron Blue

Kitchen Appliance Appraisals for Charitable Donations

When you donate kitchen appliances to a qualifying 501(c)(3) organization and the total fair market value of similar non-cash items exceeds $5,000 in a tax year, the IRS requires a qualified appraisal and a completed Form 8283 Section B to substantiate your deduction. AppraiseItNow provides certified fair market value appraisals for donated kitchen appliances, from individual high-end residential units to full commercial kitchen suites, through our equipment valuation practice.

Most appraisals are completed remotely using photographs, model numbers, serial numbers, and purchase documentation, though onsite inspection is available for large commercial installations. Our appraisers sign Form 8283 Section B and provide a fully documented report that meets IRS Publication 561 standards. Learn more about our broader charitable donation appraisals and how we support donors nationwide. Our mission is to deliver defensible, USPAP-compliant valuations with exceptional speed, professionalism, and client service.

Kitchen Appliances We Appraise for Charitable Giving

AppraiseItNow covers a wide range of donated kitchen appliances, including both residential and commercial equipment.

- Refrigerators and freezers, including French door, side-by-side, and commercial reach-in units

- Ranges, ovens, and cooktops, including gas, electric, and induction models

- Dishwashers, including residential built-in and commercial rack-type machines

- Microwave ovens, including countertop, over-the-range, and commercial convection units

- Ventilation hoods and exhaust systems for residential and commercial kitchens

- Commercial mixers, slicers, and food processors

- Coffee and espresso machines, including commercial brewers and super-automatic units

- Warming drawers, wine coolers, and beverage centers

- Combination appliance suites donated as a group to a single or multiple qualifying organizations

- High-end or luxury brand appliances such as Sub-Zero, Wolf, Viking, and Miele units where individual or aggregate values may exceed IRS thresholds

How Our Kitchen Appliance Appraisal Process Works

- Appraisals are conducted remotely in most cases, using client-submitted photos, model and serial number documentation, original purchase records, and current secondary market data. Onsite inspection can be arranged when condition verification is critical or when a large commercial installation is involved.

- Each appraisal report documents the item or group of items, describes condition, explains the valuation methodology, and provides a supported fair market value conclusion. The report is formatted to satisfy IRS requirements for a qualified appraisal under IRC Section 170(f)(11) and Treasury Regulation 1.170A-17.

- Our appraisers hold credentials through recognized professional organizations including ISA, ASA, AAA, CAGA, AMEA, and NEBB, and are qualified to sign Form 8283 Section B as required by the IRS. They carry no prohibited relationship to the donor or donee.

- Appraisals are timed to meet the IRS window: no earlier than 60 days before the donation date and no later than the due date of the tax return, including extensions. Clients who need to meet an April or October filing deadline can request expedited turnaround.

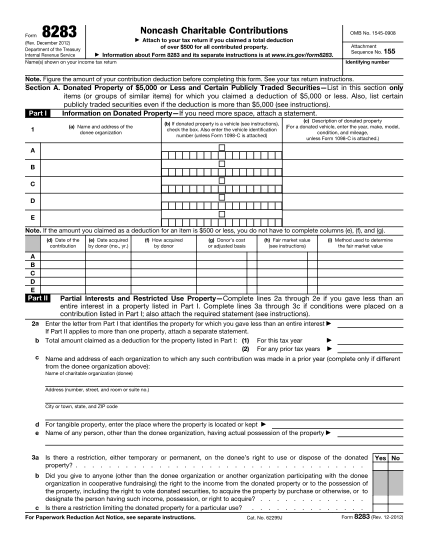

IRS Form 8283 Appraisals Required for Large Non-Cash Charitable Donations

Comprehensive qualified appraisals determining fair market value for non-cash donations exceeding $5,000, developed under USPAP standards and aligned with IRS Form 8283, Section B requirements.

What is IRS Form 8283?

IRS Form 8283, Noncash Charitable Contributions, is required when a taxpayer claims a deduction for donated property exceeding $500, and it becomes significantly more detailed when the value of donated non-cash property exceeds $5,000.

For contributions over $5,000 (other than certain publicly traded securities), the IRS generally requires a Qualified Appraisal prepared by a qualified appraiser. In these cases, the donor must complete Section B of Form 8283, and the appraiser must complete and sign Part IV (Appraiser Declaration) to confirm the appraisal meets IRS standards.

AppraiseItNow Performs 8283 Appraisals

AppraiseItNow is an expert in preparing qualified appraisals for filing of IRS Form 8283. We work with donors and their advisors to establish defensible fair market value in accordance with USPAP and IRS requirements, including support for Form 8283, Section B reporting and the appraiser declaration in Part IV.

Our credentialed appraisers provide valuation support across major asset categories, including:

- Personal Property Appraisals

- Fine Art Appraisals

- Machinery & Equipment Appraisals

- Business Valuations

- Inventory Appraisals

- Bullion & Precious Metal Appraisals

- Vehicle Appraisals

- Cryptocurrency Appraisals

Whether the asset is readily marketable or complex and illiquid, we provide independent, well-supported fair market value opinions designed to withstand scrutiny and support proper charitable reporting.

5-Star Valuation Services, Loved by Hundreds

How much does a Kitchen Appliance appraisal cost?

Appraisal Type

Standard Fee Range

Pricing By Volume

What Drives Cost?

.svg)

View all Locations

What does a kitchen appliance appraisal for charitable donation include?

A charitable donation appraisal for kitchen appliances determines the fair market value of items like refrigerators, ovens, or dishwashers being donated to a qualifying 501(c)(3) organization. The report documents condition, age, model numbers, comparable used sales, and photographs to substantiate the value claimed on IRS Form 8283 Section B. It is prepared by a qualified appraiser and meets IRS requirements for a qualified appraisal.

When do you need a kitchen appliance appraisal for a charitable donation?

A qualified appraisal is required when the aggregate fair market value of similar donated kitchen appliances exceeds $5,000 in a tax year, even if no single item reaches that threshold on its own. Donations valued between $501 and $5,000 use Form 8283 Section A without an appraisal, while donations under $500 require no Form 8283 at all. Once you cross the $5,000 threshold for similar items, Form 8283 Section B with a signed qualified appraisal is mandatory.

What credentials should the appraiser have?

The IRS requires a qualified appraiser who is independent of both the donor and the donee, has verifiable education and experience valuing similar personal property, and has no disqualifying disciplinary history. AppraiseItNow appraisers hold credentials through organizations including ASA, ISA, AAA, CAGA, AMEA, and NEBB, and all appraisals are USPAP-compliant. The appraiser signs Form 8283 attesting to their qualifications and independence.

How is fair market value determined for donated kitchen appliances?

Fair market value is the price a willing buyer would pay a willing seller for the appliances in their current used condition, with neither party under compulsion to act. Appraisers consider age, wear, depreciation from original retail price, brand, model, working condition, and comparable sales of similar used items. Non-functional or heavily damaged appliances typically yield very low fair market value.

Are AppraiseItNow's appraisals USPAP-compliant?

Yes, all AppraiseItNow appraisals are prepared in compliance with the Uniform Standards of Professional Appraisal Practice. For charitable donation purposes, our reports also meet IRS qualified appraisal requirements, including a stated valuation date, documented methodology, appraiser credentials, and a non-contingent fee declaration.

How long does a kitchen appliance appraisal take?

Most remote kitchen appliance appraisals are completed in 7 to 10 days. Onsite inspections or larger collections typically take 2 to 3 weeks. Rush service is available for same-day or next-day turnaround if your tax deadline or donation timeline requires it.

What does a kitchen appliance appraisal for charitable donation cost?

Advanced appraisals prepared for charitable donation purposes, which meet IRS qualified appraisal standards, start at $295 per item. Typical project fees range from $395 to $2,200 depending on the number of items and complexity, with volume pricing available for larger collections, for example $695 to $1,200 for around 10 items and $1,600 to $3,500 or more for 50 to 100 items. Fees are quoted as a fixed price before work begins; visit our equipment appraisal page for more detail on what drives cost.

Can you appraise kitchen appliances anywhere in the US?

Yes, AppraiseItNow provides kitchen appliance appraisals nationwide. Remote appraisals can be completed using photographs, documentation, and model information you submit from anywhere in the country, and onsite inspections can be arranged across the US when needed.

Will my appraisal be accepted by the IRS, insurers, or courts?

AppraiseItNow prepares charitable donation appraisals to meet IRS qualified appraisal standards, including a proper valuation date, documented fair market value methodology, appraiser credentials, and a non-contingent fee declaration. Following these standards significantly reduces the risk of IRS challenge on Form 8283 Section B, and USPAP-compliant reports are generally well-received by insurers and courts as well. Acceptance in any specific proceeding depends on the facts of your case, but our reports are built to withstand scrutiny.

Do multiple appliances each under $5,000 still require a group appraisal?

Yes, if you are donating several kitchen appliances that are considered similar items, such as a refrigerator, oven, and dishwasher, the IRS aggregates their fair market values across the tax year. If the combined total exceeds $5,000, Form 8283 Section B and a qualified appraisal covering all the items are required, even if no single appliance reaches $5,000 on its own.

Does the condition of donated appliances affect the appraisal value?

Condition is one of the most significant factors in determining fair market value for used kitchen appliances. Items in good working order with minimal wear will support a higher value, while non-functional or heavily damaged appliances may yield very little value and could be declined by the receiving charity. Even for items in poor condition claimed at over $500, the IRS still requires a qualified appraisal on Form 8283.

What other documentation do I need alongside the appraisal?

In addition to the qualified appraisal, you will need a written acknowledgment receipt from the 501(c)(3) charity, a completed Form 8283 Section B signed by both the appraiser and an authorized representative of the donee organization, and records such as serial numbers, acquisition history, and photographs. If you are itemizing deductions, Schedule A is also required, and for donations exceeding $500,000 in value, the full appraisal report must be submitted directly to the IRS.

When must the appraisal be dated relative to the donation?

The appraisal must be dated no earlier than 60 days before the donation date and no later than the due date of your tax return, including any extensions. An appraisal that falls outside this window does not meet IRS qualified appraisal requirements and could result in disallowance of the deduction. Timing the appraisal correctly is one of the most common compliance issues donors face.

APPRAISEITNOW APPRAISERS ARE BEST-IN-CLASS & CREDENTIALED BY LEADING APPRAISAL ORGANIZATIONS LIKE THE ISA, ASA, & MORE.