IRS-qualified appraisals for cryptocurrency donations over $5,000, meeting Form 8283 Section B requirements. AppraiseItNow provides USPAP-compliant fair market value reports for digital asset contributions, keeping your deduction defensible and audit-ready.

Best in class appraisers across asset types

.avif)

Joe Kattan

Aron Blue

Cryptocurrency Appraisals for Charitable Donations

When you donate cryptocurrency to a qualifying nonprofit and your claimed deduction exceeds $5,000, the IRS requires a qualified appraisal to substantiate fair market value under IRC §170(f)(11)(C). This requirement applies because the IRS classifies cryptocurrency as property under Notice 2014-21, not as a publicly traded security, meaning exchange prices alone are not sufficient to support your deduction. Form 8283 Section B must be completed and signed by both the qualified appraiser and the donee organization. Our personal property appraisal services cover digital assets with the same rigor we bring to tangible property.

AppraiseItNow delivers cryptocurrency appraisals online and onsite across the United States, working with donors, tax advisors, and nonprofit organizations to meet IRS timing requirements. Appraisals must be completed no earlier than 60 days before the donation date and no later than the tax return due date, including extensions. Learn more about our IRS-compliant charitable giving valuations and how we support donors at every stage. Our mission is to deliver defensible, USPAP-compliant valuations with exceptional speed, professionalism, and client service.

Cryptocurrency Types We Appraise for Charitable Giving

AppraiseItNow appraises a wide range of digital assets donated to qualifying organizations, including:

- Bitcoin (BTC) and Bitcoin forks such as Bitcoin Cash (BCH) and Bitcoin SV (BSV)

- Ethereum (ETH) and ERC-20 tokens built on the Ethereum network

- Stablecoins including USDC, USDT, and DAI when donated in large quantities

- Altcoins traded on major exchanges, including Litecoin, Cardano, Solana, and Polkadot

- Non-fungible tokens (NFTs), including digital art, collectibles, and gaming assets

- DeFi protocol tokens and governance tokens with active secondary markets

- Layer-2 tokens and wrapped assets with verifiable on-chain transaction histories

- Mined cryptocurrency with documented acquisition dates and cost basis records

- Cryptocurrency received as compensation or through staking and airdrop events

- Multi-asset crypto portfolios donated in a single transaction or across multiple transfers

How Our Cryptocurrency Appraisal Process Works

- AppraiseItNow appraisers analyze contemporaneous exchange data, on-chain transaction records, and market conditions at the time of donation to establish a defensible fair market value, going well beyond simply citing a spot price from a single exchange.

- Each completed appraisal report includes a detailed description of the donated digital assets, the valuation methodology applied, the FMV conclusion, and all information required to complete Form 8283 Section B, including the appraiser's signature and credentials.

- For donations of $500,000 or more, the full appraisal report must be attached to the tax return rather than just Form 8283, and our reports are prepared to meet that standard from the outset.

- Our appraisers hold credentials from recognized professional organizations including ISA, ASA, AAA, CAGA, AMEA, and NEBB, and all appraisals are USPAP-compliant, satisfying the qualified appraiser definition under §170(f)(11)(E)(ii).

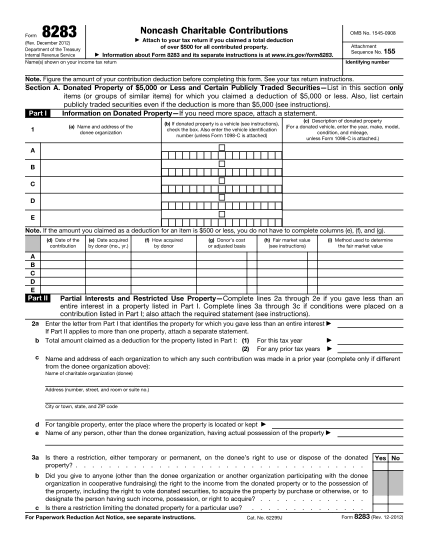

IRS Form 8283 Appraisals Required for Large Non-Cash Charitable Donations

Comprehensive qualified appraisals determining fair market value for non-cash donations exceeding $5,000, developed under USPAP standards and aligned with IRS Form 8283, Section B requirements.

What is IRS Form 8283?

IRS Form 8283, Noncash Charitable Contributions, is required when a taxpayer claims a deduction for donated property exceeding $500, and it becomes significantly more detailed when the value of donated non-cash property exceeds $5,000.

For contributions over $5,000 (other than certain publicly traded securities), the IRS generally requires a Qualified Appraisal prepared by a qualified appraiser. In these cases, the donor must complete Section B of Form 8283, and the appraiser must complete and sign Part IV (Appraiser Declaration) to confirm the appraisal meets IRS standards.

AppraiseItNow Performs 8283 Appraisals

AppraiseItNow is an expert in preparing qualified appraisals for filing of IRS Form 8283. We work with donors and their advisors to establish defensible fair market value in accordance with USPAP and IRS requirements, including support for Form 8283, Section B reporting and the appraiser declaration in Part IV.

Our credentialed appraisers provide valuation support across major asset categories, including:

- Personal Property Appraisals

- Fine Art Appraisals

- Machinery & Equipment Appraisals

- Business Valuations

- Inventory Appraisals

- Bullion & Precious Metal Appraisals

- Vehicle Appraisals

- Cryptocurrency Appraisals

Whether the asset is readily marketable or complex and illiquid, we provide independent, well-supported fair market value opinions designed to withstand scrutiny and support proper charitable reporting.

5-Star Valuation Services, Loved by Hundreds

How much does a Cryptocurrency appraisal cost?

Appraisal Type

Standard Fee Range

Pricing By Volume

What Drives Cost?

.svg)

View all Locations

What does a cryptocurrency appraisal for charitable donation involve?

A cryptocurrency charitable donation appraisal is a formal USPAP-compliant valuation that establishes the fair market value of your digital assets at the time of donation, prepared to meet IRS substantiation requirements under Section 170(f)(11). The report documents the methodology, valuation date, appraiser credentials, and all details required to support a charitable contribution deduction on your tax return. It also includes the signed appraiser declaration needed to complete Section B of Form 8283.

When is a qualified appraisal required for a cryptocurrency donation?

A qualified appraisal is required when you claim a charitable contribution deduction of more than $5,000 for donated cryptocurrency. The appraisal must be obtained no earlier than 60 days before the donation and must be in your possession before your tax return filing deadline, including extensions. Without it, the IRS will disallow the entire deduction regardless of the actual value of the assets donated.

What credentials should the appraiser have?

A qualified appraiser must hold a recognized appraisal designation from a professional organization such as ISA, ASA, AAA, CAGA, AMEA, or NEBB, or meet the minimum education and experience requirements prescribed by the IRS. They must also regularly perform appraisals for compensation and cannot receive a fee based on the appraised value of the property. AppraiseItNow appraisers hold credentials across these recognized organizations and have experience valuing digital assets for IRS-qualified purposes.

How is cryptocurrency valued for charitable donation purposes?

Cryptocurrency is valued at fair market value using market data from exchanges where the asset actively trades, adjusted in accordance with appraisal standards and accounting for factors such as volatility, the specific tokens donated, and the effective date of the donation. Simply referencing an exchange price does not satisfy the qualified appraisal requirement, because cryptocurrency exchanges do not meet the IRS definition of a qualified appraiser. The appraisal must be prepared by a credentialed individual who applies recognized methodology and documents their analysis in a formal report.

Are AppraiseItNow's appraisals USPAP-compliant?

Yes, all AppraiseItNow appraisals are fully USPAP-compliant and prepared to meet IRS qualified appraisal standards, including proper documentation of the valuation date, methodology, appraiser credentials, and a non-contingent fee declaration. For charitable donation purposes, our reports are specifically structured to satisfy the requirements of Section 170(f)(11) and support completion of Form 8283.

How long does a cryptocurrency appraisal take?

Most remote cryptocurrency appraisals are completed in 7 to 10 days. Larger or more complex portfolios requiring onsite review may take 2 to 3 weeks. Rush service is available for same-day or next-day turnaround if you have a filing deadline or donation timing to meet.

What does a cryptocurrency charitable donation appraisal cost?

Fees are fixed and quoted before work begins, with no hourly billing. Single-asset donations below $500K in USD value typically range from $295 to $595, while multiple assets or donations in the same value range run $695 to $1,200. Complex portfolios exceeding $500K in USD value are generally quoted between $1,500 and $3,000, with cost driven by factors such as:

- Number of wallets, assets, and distinct tokens included

- Complexity of chains and token types, such as Bitcoin, Ethereum, altcoins, or NFTs

- Documentation quality provided by the donor

- Differences in effective dates, token types, donees, or tax years that may require separate appraisals

Visit our personal property appraisal page for more detail, or contact us for a quote scoped to your specific holdings.

Can you appraise cryptocurrency anywhere in the US?

Yes, AppraiseItNow provides cryptocurrency appraisals nationwide. Because digital assets are documented remotely through wallet records, transaction histories, and exchange data, geography is not a barrier and most assignments are completed entirely remotely regardless of where you are located.

Will my appraisal be accepted by the IRS, insurers, or courts?

AppraiseItNow appraisals are prepared to qualified appraisal standards, including a defined valuation date, documented methodology, appraiser credentials, and a non-contingent fee declaration, all of which are required for IRS acceptance under Section 170(f)(11). Our reports are structured to support Form 8283 completion and include the appraiser signature and declaration required for donations over $5,000. While no appraiser can guarantee acceptance, following these standards closely and thoroughly documenting the appraisal significantly reduces the risk of disallowance.

Why can't I just use a crypto exchange price for my charitable donation deduction?

The IRS has determined that cryptocurrency exchanges do not qualify as qualified appraisers, so an exchange price alone cannot substitute for a formal appraisal. Cryptocurrency is also not classified as a publicly traded security, which means it does not qualify for the exception that allows publicly traded stocks to bypass the appraisal requirement. A credentialed appraiser must prepare a formal report to satisfy the substantiation rules for donations over $5,000.

What information needs to appear on Form 8283 for a large cryptocurrency donation?

For noncash donations over $5,000, you must complete Section B of Form 8283, which requires the qualified appraiser to sign and date the report, provide a declaration acknowledging the appraisal will be used on a tax return, and confirm they have not been barred from presenting evidence before the IRS in the past three years. The form must also include a detailed description of the cryptocurrency, the fair market value, acquisition information, and a statement from the charitable organization. For donations of $500,000 or more, the full qualified appraisal must be attached directly to your tax return, not just the form.

What happens if I skip the qualified appraisal for a crypto donation over $5,000?

The IRS will disallow your entire charitable contribution deduction if you fail to provide a qualified appraisal for a cryptocurrency donation exceeding $5,000. The reasonable cause exception does not apply to this requirement, so there is no fallback argument available if the appraisal is missing. Courts have consistently upheld this position, emphasizing that Form 8283 itself provides clear notice that substantial noncash donations must be supported by a formal appraisal.

Do I need to attach the full appraisal to my return for a very large crypto donation?

For donations of $500,000 or more, yes, the complete qualified appraisal must be attached to your tax return itself. For donations between $5,000 and $500,000, you file Form 8283 with your return but are not required to attach the full appraisal document, though you must retain it in your records in case of an audit.

APPRAISEITNOW APPRAISERS ARE BEST-IN-CLASS & CREDENTIALED BY LEADING APPRAISAL ORGANIZATIONS LIKE THE ISA, ASA, & MORE.