Charitable Donation appraisals in North Carolina for personal property, equipment and machinery, fine art, business interests, boats and watercraft, automobiles and vehicles, and inventory. AppraiseItNow provides credentialed, USPAP-compliant Charitable Donation appraisals online and onsite across North Carolina, including Charlotte, Raleigh, and Greensboro.

.png)

Credentialed, best-in-class appraisers across assets

.avif)

Joe Kattan

Anne Hay, ISA AM

Jason Dolph, CAGA

Ashley Innes, ISA AM

Justin Ramirez, ASA, ABV, CFA

Marnie Erkelens, CAGA

Raymond Ghelardi, ASA

Aron Blue

Frequently Asked

Questions

No Frequently Asked Questions Found.

About Charitable Donation Appraisals in North Carolina

AppraiseItNow provides qualified charitable donation appraisals for North Carolina donors who need to substantiate non-cash contributions to the IRS. Federal rules require a qualified appraisal for donations exceeding $5,000 per item or group of similar items, with IRS Form 8283 Section B completed and signed by both the appraiser and the donee organization. Donations of art valued at $20,000 or more, or total donated property exceeding $500,000, require the full appraisal report attached to the tax return. Our mission is to deliver defensible, USPAP-compliant valuations with exceptional speed, professionalism, and client service.

Both remote and onsite appraisal options are available, making it easy for donors across the state to get the documentation they need. Our appraisal services in North Carolina cover everything from urban centers like Charlotte and Raleigh to coastal communities and rural regions statewide.

What Does AppraiseItNow Appraise for Charitable Donation in North Carolina?

AppraiseItNow covers all major asset classes commonly donated to qualifying organizations in North Carolina, including:

- Personal Property, including jewelry, antiques, furniture, coins, collectibles, and household goods

- Equipment & Machinery, including medical equipment, restaurant equipment, manufacturing machinery, and technology assets

- Fine Art, including paintings, prints, sculpture, photography, and mixed media

- Business Interests, including LLCs, S-corps, partnerships, fractional interests, and privately held stock

- Boats & Watercraft, including sailboats, powerboats, yachts, jet skis, and personal watercraft

- Automobiles & Vehicles, including cars, trucks, motorcycles, RVs, trailers, and classic vehicles

- Inventory, including retail inventory, wholesale stock, raw materials, and finished goods

Who Does AppraiseItNow Serve in North Carolina for Charitable Donation?

AppraiseItNow serves individual donors, high-net-worth households, business owners, and estate representatives across North Carolina who are contributing non-cash assets to universities, museums, nonprofits, and other qualifying organizations. This includes donors giving fine art to institutions like UNC Chapel Hill, equipment to community organizations, boats to maritime nonprofits, and collectibles or vehicles to charitable causes throughout the state.

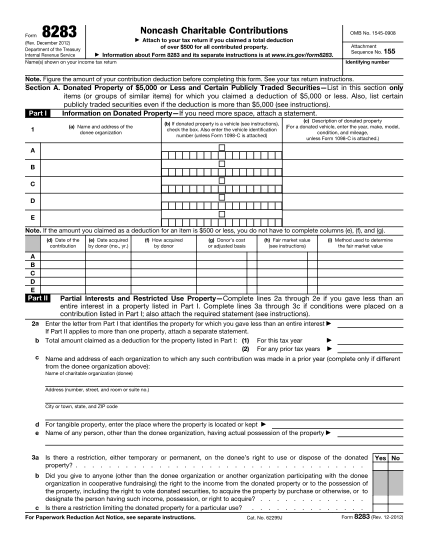

IRS Form 8283 Appraisals Required for Large Non-Cash Charitable Donations

Comprehensive qualified appraisals determining fair market value for non-cash donations exceeding $5,000, developed under USPAP standards and aligned with IRS Form 8283, Section B requirements.

What is IRS Form 8283?

IRS Form 8283, Noncash Charitable Contributions, is required when a taxpayer claims a deduction for donated property exceeding $500, and it becomes significantly more detailed when the value of donated non-cash property exceeds $5,000.

For contributions over $5,000 (other than certain publicly traded securities), the IRS generally requires a Qualified Appraisal prepared by a qualified appraiser. In these cases, the donor must complete Section B of Form 8283, and the appraiser must complete and sign Part IV (Appraiser Declaration) to confirm the appraisal meets IRS standards.

AppraiseItNow Performs 8283 Appraisals

AppraiseItNow is an expert in preparing qualified appraisals for filing of IRS Form 8283. We work with donors and their advisors to establish defensible fair market value in accordance with USPAP and IRS requirements, including support for Form 8283, Section B reporting and the appraiser declaration in Part IV.

Our credentialed appraisers provide valuation support across major asset categories, including:

- Personal Property Appraisals

- Fine Art Appraisals

- Machinery & Equipment Appraisals

- Business Valuations

- Inventory Appraisals

- Bullion & Precious Metal Appraisals

- Vehicle Appraisals

- Cryptocurrency Appraisals

Whether the asset is readily marketable or complex and illiquid, we provide independent, well-supported fair market value opinions designed to withstand scrutiny and support proper charitable reporting.

5-Star Valuation Services, Loved by Hundreds

Does AppraiseItNow handle charitable donation appraisals in North Carolina?

Yes, AppraiseItNow provides qualified appraisals for charitable donation purposes throughout North Carolina. Whether you are donating to a local nonprofit, a conservation organization, or a national charity, we can help you meet IRS requirements and document your contribution properly.

What kinds of assets can be appraised for a charitable donation in North Carolina?

We appraise a wide range of assets for charitable donation purposes, including artwork, antiques, collectibles, jewelry, vehicles, boats, business interests, equipment, and inventory. Our appraisers have experience across many asset categories, so most personal property and tangible assets can be covered.

Are your charitable donation appraisals USPAP compliant?

Yes, all appraisals completed by AppraiseItNow follow the Uniform Standards of Professional Appraisal Practice (USPAP). This compliance is required for a qualified appraisal under IRS rules and ensures your report will hold up to scrutiny.

Why would someone in North Carolina specifically need a charitable donation appraisal?

North Carolina has an active conservation community, with many landowners donating to land trusts and conservation organizations, and the state also offers its own tax credit provisions for certain property donations under North Carolina law. Beyond conservation, donors across the state give artwork, vehicles, business assets, and collections to nonprofits and need a qualified appraisal to substantiate their federal deduction. Having a properly documented appraisal protects you whether you are filing with the IRS or claiming a state credit.

Can I get a charitable donation appraisal remotely if I am in North Carolina?

Absolutely. AppraiseItNow offers remote and online appraisal services, so you do not need to schedule an in-person visit. You can submit photos and documentation digitally, and our appraisers will complete a qualified appraisal that meets IRS standards.

How is pricing determined for a charitable donation appraisal?

Fees depend on the asset type and the scope of the appraisal. Visit our pricing page for ranges or contact us directly.

How long does it typically take to receive a completed charitable donation appraisal?

Turnaround times vary by asset type:

- Vehicles: 3 to 5 days

- Personal property and equipment: 7 to 10 days

- Artwork: 5 to 7 days for simple projects, 2 to 3 weeks for complex assignments

- Business valuations: 2 to 4 weeks

- Inventory: 2 to 4 weeks

Who actually prepares the appraisal report?

Your report is prepared by a qualified appraiser with recognized credentials and demonstrated experience valuing the specific type of property being donated. Every appraiser on our platform meets IRS requirements for qualified appraisers, including independence from the donor and donee.

Are there any North Carolina-specific rules I should know about for charitable donation appraisals?

North Carolina has a unique provision under Session Law 2007-309 and G.S. 105-153.11 that allows taxpayers claiming state tax credits for fee simple donations of property to conservation purposes to submit the county appraised value, adjusted by the sales assessment ratio, in place of a full appraisal report. For federal deductions, however, a qualified appraisal is still required for donations exceeding $5,000, and county tax values do not satisfy that requirement. A USPAP-compliant self-contained appraisal remains an option for state credit purposes as well.

What information do I need to provide to get started?

To begin, it helps to have a description of the asset, any documentation of provenance or ownership, photographs if available, and the name of the receiving charity. The more detail you can share upfront, the faster we can match you with the right appraiser and begin the process.

Will a charitable donation appraisal from AppraiseItNow be accepted by the IRS?

Yes. Our appraisals are prepared by qualified appraisers following IRS requirements and USPAP standards, which are the benchmarks the IRS uses when reviewing charitable contribution deductions. A properly completed appraisal, paired with IRS Form 8283 filed with your return, gives you the documentation needed to support your deduction.

If I donate to a North Carolina conservation organization, can I just use my county's tax value instead of hiring an appraiser?

For federal tax deductions, no. County appraisals do not substitute for a qualified appraisal when your donation exceeds $5,000. For North Carolina state tax credits on fee simple donations to conservation purposes, the county appraised value adjusted by the sales assessment ratio may be submitted in place of a full report, but a USPAP-compliant appraisal is always an acceptable alternative.

I am donating a collection of similar items to multiple North Carolina charities. Do I need a separate appraisal for each one?

One qualified appraisal can cover similar items donated to multiple charities, since the IRS aggregates similar items across donees when determining whether the $5,000 appraisal threshold is met. You will, however, need a separate IRS Form 8283 Section B completed for each donee, with the appraiser's and donee's signatures on each form.

What is the difference between the appraisal summary on my tax return and the full qualified appraisal?

The appraisal summary is the completed IRS Form 8283 Section B that you attach to your tax return for donations over $5,000, signed by both the appraiser and the donee. The full qualified appraisal is the detailed supporting document you must retain but generally do not submit unless the donation involves artwork valued at $20,000 or more, or other property valued at $500,000 or more. The IRS reviews the summary when processing your return and requests the full appraisal during audits or for high-value items.

At what dollar amount does a charitable donation of a vehicle, boat, or artwork require a qualified appraisal in North Carolina?

A qualified appraisal is required when the donated item or group of similar items exceeds $5,000 in value, which is the federal threshold that applies in North Carolina. One exception applies to vehicles and boats: if the charity sells the item without significant use or improvement, your deduction is limited to the gross sales proceeds and no appraisal is needed. For artwork valued at $20,000 or more, the full appraisal must be attached directly to your tax return.

Do I need an appraisal if I am donating used clothing or household goods to a North Carolina nonprofit?

Generally, no. Used household items and clothing valued at $5,000 or less in aggregate fall under IRS Form 8283 Section A and do not require a qualified appraisal. The one exception is if any individual item is not in good used condition or better and is valued over $500, in which case an appraisal must accompany your return.

How close to my donation date does the appraisal need to be completed?

The qualified appraisal must be conducted no earlier than 60 days before the donation date and no later than the due date of your tax return, including any extensions, and you must receive it before filing. The valuation effective date can be set to the gift date even if the appraisal is completed shortly after. These federal timing rules apply uniformly to North Carolina donors.

APPRAISEITNOW APPRAISERS ARE BEST-IN-CLASS & CREDENTIALED BY LEADING APPRAISAL ORGANIZATIONS LIKE THE ISA, ASA, & MORE.