When a person passes away, their executor is tasked with managing the estate—a responsibility that often involves a home, artwork, jewelry, and other assets accumulated over a lifetime. This raises two critical questions. What is everything worth? And why does that value matter?

The answer lies in a date of death appraisal. Whether you are settling an estate for the first time or are a professional handling these matters, understanding this valuation is key to avoiding tax penalties, family disputes, and costly errors.

A date of death appraisal is a professional report that establishes the fair market value of an asset on the specific date the owner passed away. Unlike a standard appraisal that reflects today’s prices, this valuation “freezes” the value at that moment in time, creating a definitive financial snapshot of the estate.

This appraisal must be conducted by a qualified appraiser who adheres to the Uniform Standards of Professional Appraisal Practice (USPAP). These national standards ensure the final report is credible, defensible, and suitable for all legal and tax purposes.

You might wonder if you can just estimate values yourself. For official purposes, the answer is no. A professional appraisal is non-negotiable for two primary reasons: fulfilling tax obligations and ensuring a fair, legal settlement of the estate.

First and foremost, appraisals are required for tax compliance. If an estate is large enough to trigger federal estate taxes, the IRS requires a detailed filing on Form 706 with precise valuations for all assets. Many states also impose their own estate or inheritance taxes with much lower exemption thresholds, meaning an appraisal may be necessary even if no federal tax is due.

Key Takeaway: An accurate appraisal establishes the “step-up in basis,” potentially saving heirs thousands of dollars in future capital gains taxes when they sell an inherited asset.

Furthermore, an appraisal establishes the “step-up in basis” for inherited assets—a crucial tax benefit. For example, if your mother bought a painting for $5,000 that was worth $50,000 on her date of death, your tax basis becomes $50,000. If you later sell it for $52,000, you only pay capital gains tax on the $2,000 gain. Without an appraisal to document this, you could be taxed on the entire $47,000 of appreciation. Executors must report this basis to the IRS and beneficiaries on Form 8971.

Second, appraisals are vital for a fair and legal estate settlement. As an executor, you have a fiduciary duty to manage assets responsibly. Using a qualified appraiser protects you from claims of mismanagement or favoritism. It also ensures the equitable distribution of assets among heirs, preventing family disputes when one person inherits property and another receives assets of a different kind.

While assets like bank accounts have clear values, most other property requires a professional opinion. The most common asset is real property, which includes the primary residence, vacation homes, rental properties, undeveloped land, and commercial buildings.

Next is tangible personal property, which often holds significant and specialized value. This broad category includes fine art, antiques, jewelry, and collectibles like coins or stamps. It also covers classic automobiles, boats, valuable musical instruments, and collections of items such as fine wine or firearms.

Finally, business and financial assets without a public market price must be professionally valued. This includes interests in a closely held company, partnership shares, LLC memberships, and intellectual property like patents or royalty streams.

The IRS has specific requirements that a date of death appraisal must meet to be considered valid. A compliant report must be performed by a “qualified appraiser,” defined as a professional with verifiable credentials, education, and experience in valuing the specific type of property in question. A real estate appraiser, for instance, is not qualified to appraise fine art.

Important: The IRS requires appraisals to be based on “fair market value”—the realistic price a willing buyer would pay a willing seller. This is not the same as replacement or insurance value.

The valuation itself must be based on “fair market value”—the price a willing buyer would pay a willing seller in an open market. This is not the same as replacement or insurance value. The report must also be thoroughly documented with detailed descriptions, the methodology used, and supporting market data. Vague opinions are not acceptable; the conclusion must be supported by evidence.

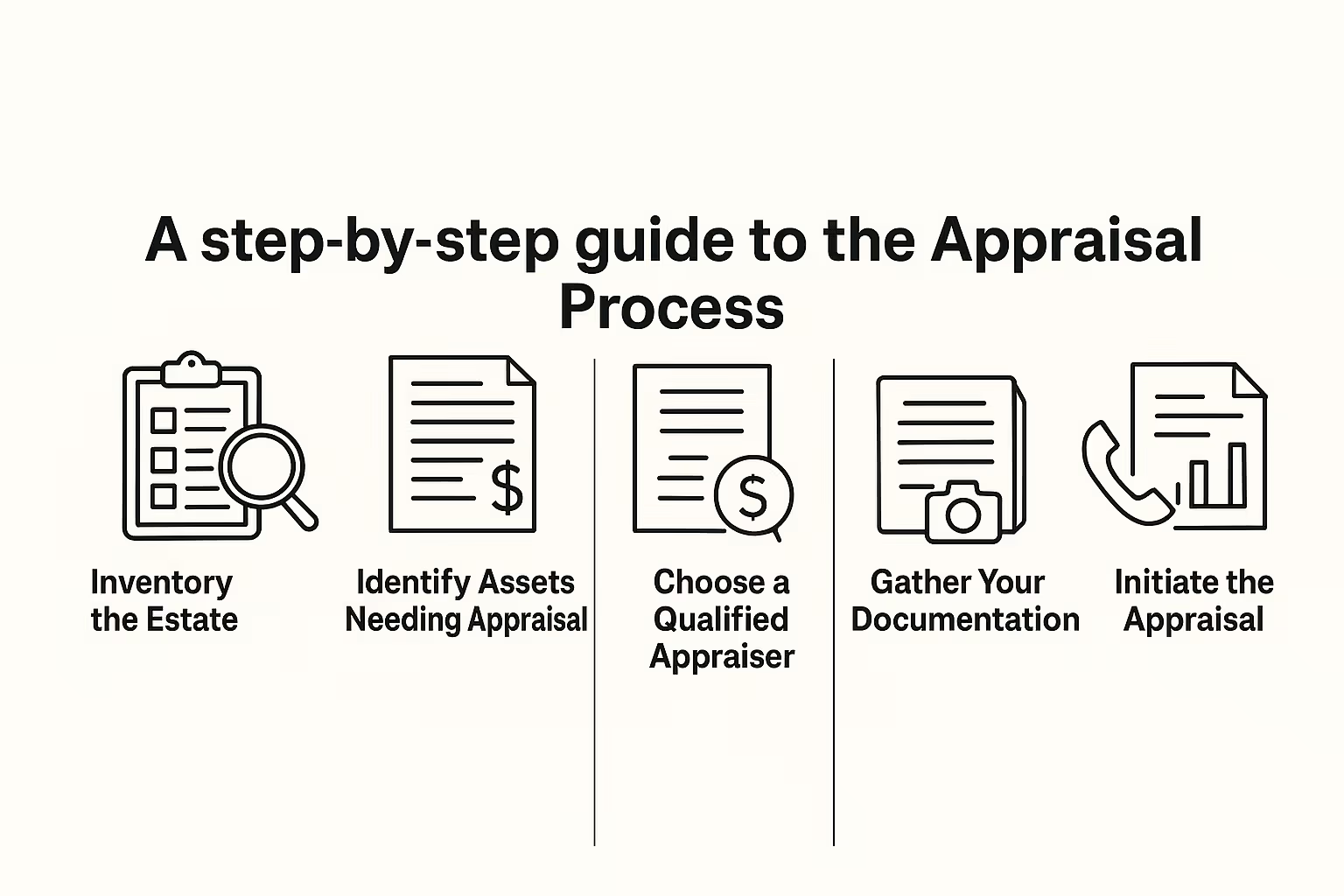

Navigating the appraisal process can be straightforward if you follow a few key steps.

When handling valuations, executors can fall into several traps. One of the most frequent errors is relying on an outdated appraisal. A valuation from several years ago is irrelevant, as the IRS requires the fair market value on the specific date of death. Another mistake is using online estimators or your local property tax assessment; these are not substitutes for a formal appraisal and will be rejected by tax authorities.

Warning: Using an appraiser without the proper credentials or expertise for a specific asset will result in an invalid report, wasting both time and money.

It is also critical to choose a qualified appraiser with expertise in the specific asset class you need valued. Using a generalist for specialized items creates an invalid report. Be sure to avoid waiting too long to start the process, as it becomes harder to find comparable sales data from the past. Finally, remember to separate sentimental value from fair market value. An appraiser’s job is to provide an objective, evidence-based valuation, not one influenced by personal attachment.

Q: How much does a date of death appraisal cost?

A: Costs vary based on the asset’s complexity. You can review our general pricing information for an idea, but a single-item appraisal may start around $195, while a complex estate can cost several thousand dollars.

Q: Can the appraisal be done remotely?

A: Yes, for many types of personal property. Online appraisals that meet USPAP and IRS standards are possible with clear photos and documentation. Some assets, like high-value jewelry, may require an in-person inspection.

Q: What happens if the IRS challenges my appraisal?

A: This is why using a qualified appraiser who follows USPAP is so important. A well-documented, professional report is highly defensible. If challenged, the IRS may request more information or conduct its own appraisal.

A date of death appraisal is more than just paperwork—it is financial protection for executors, tax savings for beneficiaries, and peace of mind for families. It ensures you meet your legal obligations, prevent disputes, and allow everyone to move forward with confidence.

At AppraiseItNow, we understand that settling an estate is a difficult and time-sensitive process. Our nationwide network of vetted, credentialed appraisers provides USPAP-compliant reports that meet all IRS requirements. Our efficient online platform makes it easy to submit your request and receive a defensible report, often within one to two weeks.

Ready to get started? Contact us today for a consultation and a transparent quote. We’ll match you with the right expert to ensure you have the documentation you need to request an appraisal and settle the estate properly.